Small extra mortgage payments can make a big difference over time by helping reduce interest and shorten your amortization.

|

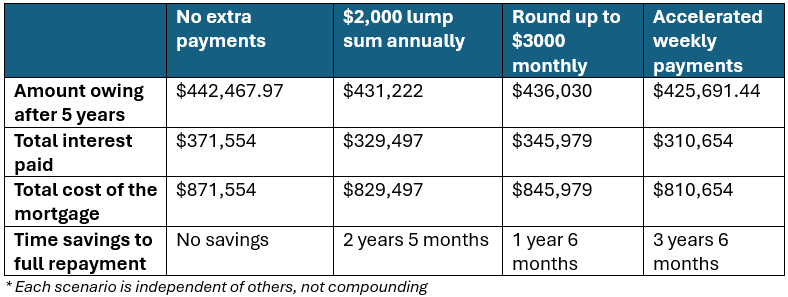

Having some extra cash on hand might give you some breathing room on rising gas and food prices, building an emergency fund, or even the ability to make a big purchase you’ve delayed. But – should you pay down your mortgage instead? If you’re considering paying down your mortgage, you’re in luck, because today we’re going to look at how a lump sum payment can transform your mortgage future. Base Case Scenario Here we’re going to look at a mortgage with a $500,000 balance at a rate of 4.99% and a 25-year amortization. In this scenario, your monthly payment would be $2,905.18. If we fast forward 25 years to the end of that mortgage, having made no lump sum payments, you’ll have paid $371,554 in interest and a total of $871,554 in payments for your $500,000 mortgage. Although your rate will vary over the course of your mortgage, in this example we’re going to keep it consistent at 4.99%. Payment Options When we’re talking about paying down your mortgage early, there are three main ways you can do this. The first is to save a lump sum of cash, which you put down all at once, one time per a year (for example, on your mortgage anniversary). You don’t have to make this payment every year, but you likely have the option to put down a flexible amount of cash with upper and lower limits every year of your mortgage. The second option is to round up your regular payments to a set amount. Again, there will be upper and lower limits on how much you can pre-pay, but you’ll likely be able to round up by a couple hundred dollars or to the nearest $100, for example. The third option is to go with accelerated payments, which are normally offered weekly or bi-weekly. Here the lender will calculate the specific amount for you. Each of these options will help you pay less in interest over the lifetime of your mortgage, with varying impact on the total amount of interest. Below is a chart showing how these three prepayment types can change your mortgage.

|

|

|

As you can see, even a small monthly increase in your payment can save you tens of thousands of dollars on your mortgage. The biggest impact you can make on your own financial future is to change your payment frequency – the more often you pay, the less interest you pay, and the sooner you pay off your mortgage in full! Even if you don’t have a new mortgage, you can start any of these strategies at any time. Whenever you do start prepaying, you’ll start saving time and money over the rest of the term of your mortgage. Be Aware: It’s important to consult your lender about what prepayment types and amounts allowed within your current mortgage. Many lenders set prepayment amounts as a percentage of your outstanding mortgage balance, although some lenders offer more unique options like doubling a payment. If you want to run this scenario for your own mortgage, with whatever numbers you have, and different prepayment amounts, I’ve got great news. You can download my app and do it all – easily and for free – whenever you want. And if you have questions, you can DM or call me right in the app for help! |